Markets Struggle in Q1 Amid Policy Uncertainty and Trade War Concerns

Volatility gripped markets in the first quarter of 2025 and the major stock indices saw significant declines as chaotic U.S. trade and tariff policies caused a steep plunge in business and consumer confidence, which raised concerns that economic growth would dramatically slow and corporate earnings growth would disappoint.

Stocks started the new year by extending the declines of late 2024, as worries the Federal Reserve could pause interest rate cuts weighed on the markets early in January. However, solid economic data, encouraging inflation readings and positive commentary from Fed officials about future rate cuts pushed back on those fears, and the S&P 500 recovered much of those initial losses by mid-month. Additionally, stocks rallied into and following Inauguration Day, as investors anticipated a “pro-growth” administration taking power while fears of dramatic tariffs on “Day One” of the Trump presidency went unfulfilled. The S&P 500 hit a new all-time high shortly after President Trump’s inauguration, and the rally continued into late January after the Fed signaled it still expected to cut rates in 2025, further calming fears of a pause in rate cuts. However, at the very end of January, investors got a preview of looming tariff/trade volatility when President Trump threatened 25% tariffs on Colombia. However, those tariffs were not ultimately implemented, so markets largely ignored them and stocks finished January with a solid gain.

Trade and tariff policy became a major influence on markets in February, however, and dramatically increased market volatility by month-end. During the first few days of February, President Trump threatened and then delayed 25% tariffs on Mexico and Canada, which temporarily spiked market volatility. However, the one-month delay of those tariffs led markets to believe that President Trump was using tariff threats as a negotiating tactic and that substantial tariffs would not be implemented after all. That sentiment helped to ease investor concerns while economic data remained solid. Those factors combined to send the S&P 500 to a new all-time high on February 19th. However, the rally would not last. In late February, consumer confidence declined dramatically, and some economic reports implied the trade and tariff uncertainty was starting to slow economic growth. Those fears were reinforced when the Atlanta Fed’s GDPNow turned negative, implying economic growth may be stalling. Meanwhile, tariff threats and general policy volatility continued through the end of the month and that, combined with plunging consumer sentiment, sparked a “growth scare” amongst investors that weighed on stocks and sent the S&P 500 marginally lower in February.

The market declines accelerated in March as President Trump made good on his threat to implement 25% tariffs on Mexico and Canada (and an additional 10% tariff on China). President Trump delayed some of those tariffs on Mexico and Canada until early April, but many other tariffs were left in place, and that shattered investors’ belief that tariff threats were just a negotiating tactic. Meanwhile, several corporations from various sectors began to lower earnings guidance, citing reduced consumer spending and business investment. Those guidance cuts reinforced fears that policy uncertainty could cause an economic slowdown, and the S&P 500 fell to a six-month low. In late March, markets tried to rebound amidst a lull in tariff threats, but it didn’t last as President Trump announced 25% auto tariffs on March 26th, sending stocks lower once again. The S&P 500 finished the quarter near the year-to-date lows.

First Quarter Performance Review

Market internals revealed that while the S&P 500 posted a negative return for the quarter, the declines in the index were mostly due to sharp drops in widely held technology and consumer stocks, as other parts of the market proved resilient.

To that point, on a sector level, only four of the 11 S&P 500 sectors finished the quarter with a negative return and two of those four sectors saw only fractional declines. As mentioned, the consumer discretionary and tech sectors were, by far, the worst-performing sectors in the first quarter as both saw substantial declines. And, since those two sectors carry some of the largest weights in the S&P 500, they weighed on the overall index performance. The consumer discretionary sector was the worst performer for the quarter as it was hit by intense weakness in one of the largest consumer stocks (Tesla) combined with general concerns about lower consumer spending in the face of policy uncertainty. The technology sector was the other substantially negative performer in the first quarter as tech stocks fell following the debut of the Chinese AI program DeepSeek, which challenged assumptions about the future economic benefit of AI for major tech firms.

Looking at sector outperformers, energy was the top-performing sector in Q1, thanks to rising demand expectations following strong Chinese economic data and after some European countries committed to increasing debt to fund economic growth. The healthcare, utilities, and consumer staples sectors logged modest gains in Q1, as those traditionally defensive sectors were viewed as more insulated from any new trade wars and tend to be more resilient in the face of an economic slowdown.

From an investment style standpoint, value significantly outperformed growth in Q1, as growth strategies posted substantial losses due to their large weightings of tech and consumer stocks. Value strategies logged a slightly positive return over the past three months and benefited from exposure to a broader array of sectors that traded at lower valuations and were not as impacted by the negative headlines in the first quarter.

Finally, looking at performance by market cap, small caps declined sharply in the first quarter and lagged large caps thanks to a combination of rising worries about economic growth and still high interest rates. Large cap indices also declined in the first quarter, although those losses were more modest.

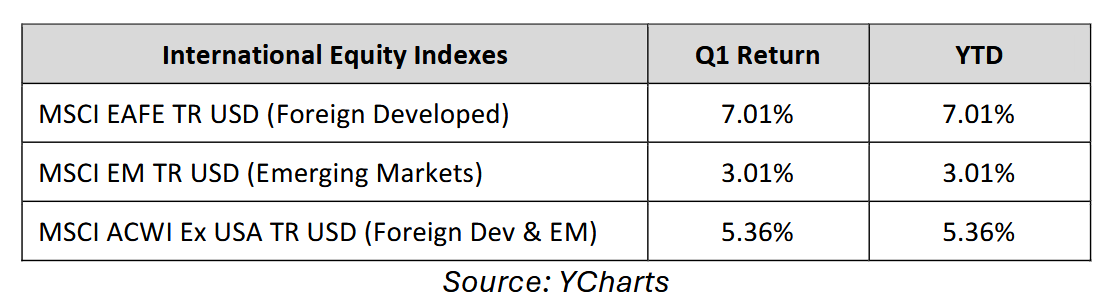

Internationally, foreign markets massively outperformed the S&P 500 and finished the quarter with a substantially positive return. Foreign developed markets saw the largest gains and outperformed emerging markets after Germany and other EU countries signaled a willingness to increase deficit spending to boost economic growth and defense. Emerging markets logged more modest gains thanks to better-than-expected Chinese economic data.

Commodities were modestly positive in the first quarter, as strength in gold helped to boost the major commodity indices. Gold hit a new record high and traded above $3000/oz. thanks to a weaker U.S. dollar and increased demand following policy volatility from the new administration. Oil logged a small loss but finished well off the lows of the quarter thanks to better-than-expected Chinese economic data and expectations for more demand from Europe.

Switching to fixed income markets, the leading benchmark for bonds (Bloomberg Barclays US Aggregate Bond Index) realized a modestly positive return for the first quarter of 2025. Better-than-expected inflation readings and general concerns about economic growth boosted bonds broadly and helped longer-duration bonds to outperform shorter-duration bills and notes, as investors sought higher long-term yields amidst policy uncertainty.

Switching to fixed income markets, the leading benchmark for bonds (Bloomberg Barclays US Aggregate Bond Index) realized a modestly positive return for the first quarter of 2025. Better-than-expected inflation readings and general concerns about economic growth boosted bonds broadly and helped longer-duration bonds to outperform shorter-duration bills and notes, as investors sought higher long-term yields amidst policy uncertainty.

Turning to the corporate bond market, higher-quality but lower-yielding investment-grade bonds outperformed higher-yielding but lower-quality bonds in the first quarter, and that reflected investor concerns about future economic growth amidst policy uncertainty. However, both investment-grade and high-yield corporate bonds finished the first quarter with modest gains, reflecting a still present sense of economic optimism from bond investors.

Second Quarter Market Outlook

Stocks begin the second quarter of 2025 following the worst quarterly performance in nearly three years and facing dual market headwinds of policy uncertainty and potentially slowing economic growth. However, while clearly markets are facing legitimate headwinds, it’s important to realize that stocks fell in the first quarter mostly on fears of what might happen in the economy, not because of what is actually occurring. Point being, if future policy decisions and an economic slowdown aren’t as bad as currently feared, it could cause a substantial market rebound in the coming months.

Starting with trade and tariff policy, there can obviously be improvement in the communication strategy from the administration regarding its policy goals and there were signs late in the first quarter that officials realized their errors and were working to communicate more directly, effectively and consistently with markets. Regardless of what actual tariff policy ultimately looks like, improvement in communication of the administration’s policy goals will be a market positive and could help end this pullback.

Turning to economic growth, while fears of a slowdown surged in the first quarter, economic data stayed mostly resilient. Jobless claims remained subdued, measures of manufacturing and service activity showed continued expansion and the unemployment rate remained historically low, close to 4.0%. Put simply, there was little in the actual data in Q1 to imply the economy is weakening. If economic data stays solid throughout the second quarter, it will push back on those recession fears and could help fuel a rebound in the markets.

On market valuation, the declines of the first quarter have resulted in the S&P 500 trading at a more reasonable valuation compared to the start of the year, as extremely bullish investor sentiment has been replaced by a decidedly bearish outlook (which has historically set the stage for a market rebound). Bottom line, the market was richly valued at the start of the year and investor sentiment was complacent, but the volatility of the first quarter has removed both of those conditions and that is a general positive for the markets.

Finally, while the S&P 500 suffered moderate declines in the first quarter, there were many parts of the market that weathered the volatility and posted positive returns. More than half of the sectors within the S&P 500 logged positive returns in the first quarter while two other sectors only saw slight declines, underscoring that the volatility we witnessed in the first quarter didn’t result in a broad market wipeout and there are sectors and factors that can continue to outperform in this environment.

Bottom line, the first quarter did contain several negative surprises for investors and we begin the second quarter with significant uncertainty on trade policies and legitimate concerns about future economic growth. But there are also positive factors at work that must be considered, including a still-resilient economy and looming positive economic policies such as deregulation and potential tax cut extensions. So, despite depressed investor sentiment, the outlook for the economy and markets is not universally negative.

At TCM Wealth Advisors, we have experienced these types of markets before and are committed to helping you effectively navigate this challenging investment environment. Successful investing is a marathon, not a sprint, and through both bull and bear markets, we will remain focused on providing a risk managed approach to help meet your long-term investment goals.

We remain vigilant towards risks to client portfolios and the economy, and we thank you for your ongoing confidence and trust. Please rest assured that our team will remain dedicated to helping you successfully navigate this volatile market environment.

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio review.

We are a Fee-Only Fiduciary financial planning and investment advisory firm that individuals and small businesses in the Akron/Cleveland area and throughout the United States trust with their financial future. Our team will work with you to create a personalized financial blueprint. To begin your journey towards a successful and stress-free financial future, please give us a call at 330-836-7000 to schedule an introductory conversation. Alternatively, you may also schedule an introductory conversation with us here.

Since 2004, TCM Wealth Advisors has been providing Fee-Only Fiduciary Advice to our clients in Northeast Ohio (Akron/Canton, Cleveland), and around the country.